The general rise of new energy vehicles has exceeded many people’s expectations, just as the crazy growth of power battery raw materials has also exceeded many people’s expectations.

The automobile industry is facing a new pricing logic: the scarce upstream mineral resources are not only affected by the industry cycle but also mixed with increasingly heavy financial attributes-behind this pricing logic, the upstream and downstream of the automobile industry chain are struggling for the right to speak.

The past three months have witnessed two things: in the Chinese market, the average price of battery-grade lithium carbonate has soared to 500,000 yuan/ton, a 10-fold increase in one year, and the supply is in short supply; on the London Metal Exchange, the price of nickel has skyrocketed by more than 240%, broke through 100,000 US dollars per ton, and later corrected to 40,000 US dollars, which was still twice the price at the beginning of the year. Lithium and nickel are both important raw materials for new energy vehicle power batteries.

The pressure for sharply rising prices of raw materials has spread from battery makers to automakers and then to consumers. In March, new energy vehicle companies lined up to raise prices. It is said that two-thirds of the top 30 new energy vehicles in sales have officially announced price increases, and the remaining one-third are on the way to increasing prices. The reasons are similar: due to “rising raw material prices”.

There was a wave of price hikes for new energy vehicles at the beginning of this year. At the end of January, BYD announced that due to factors such as rising raw material prices and the decline of subsidies for new energy car purchases, the standard price of many new energy models will be raised by 1,000-7,000 yuan. Tesla, XPeng Motors, Neta Automobile, GAC Aian, etc. have also followed up on the price increase.

“The sales of car companies that raised prices in January are still strong, they have not fallen behind, and there are even some pulling effects.” Cui Dongshu, secretary-general of the Passenger Federation, said in an interview with Sohu Auto. Represented by Tesla, BYD, and XPeng Motors, for new energy car companies, orders did not drop but rose after the price increase. Raising prices has instead prompted consumers to make decisions in advance, and raising prices has become a promotional tactic.

Even if the follow-up sales slow down, “BYD and Tesla” who have raised prices first already hold tens of thousands of orders. This makes it inevitable for the car companies that are still on the sidelines to raise along.

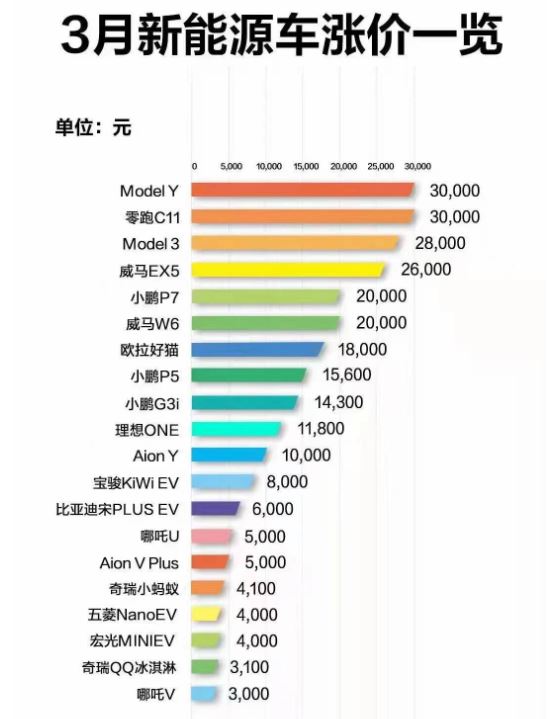

If the price increase in January is just a few car companies “testing the water”, then the price increase in March is more “forced”. In addition to Tesla and BYD, Leapmotor, XPeng, Weimar, Wuling, Ora, Ideal, Neta, Chery, and other new energy vehicles have adjusted their prices and the increase is mostly by 3%-5%, from 2,000 to 30,000. “One hour of electricity increases by 200-300 yuan. If car companies do not increase prices, they will be passive. The price increase depends on whether consumers can accept it.” Cui Dongshu said.

Even if prices are going to increase, how and how much is still a problem.

Taking BYD as an example, most of its low-priced models will increase by about 3%, pure electric models will increase by 4-5%, and the prices of high-end models have basically remained unchanged. “BYD also hopes to seize more market space for high-end prices through this round of price adjustment.” A BYD sales consultant said that the price increase of the DM-i car series will not affect sales, after all, there are no competitors in this market.

In contrast, a series of electric cars that were very popular last year, Neta, Baojun, Ora, etc. have successively increased their prices this year, ranging from more than 3,000 to nearly 20,000 yuan. When the price/performance ratio is reduced, can these cars still sell? Great Wall Ora Black and White Cat have announced that it will stop taking orders and plans to launch products in the price range of 150,000 to 300,000 this year. Soaring raw material prices will only accelerate automakers to devote more resources to more profitable mid-to-high-end models.

“It was predicted that the price of power batteries would increase this year, but I didn’t expect it to increase so much, beyond imagination.” He Xiaopeng, chairman of XPeng Motors, said recently, “Due to the increase in the price of power batteries, the larger the battery scale of car companies, the proportion of price increases. The higher it is.” He believes that the current price increase of XPeng Motors is within a reasonable range, and this year, its production capacity will mainly be placed on models with higher gross profit.

Up to now, except for Tesla, most of the car companies that have officially announced price increases are Chinese new car companies and traditional independent brands. Only the Volkswagen I.D series of joint ventures has increased by 5,400 yuan. Cui Dongshu believes that the penetration rate of new energy vehicles in mainstream joint venture car companies is only 3%, and joint venture brands have the ability to absorb costs, and there will be no significant price hike in the future. However, the proportion of new energy in independent brands has reached 38%, and battery price fluctuations have a greater impact on independent brands

Usually, it is a cautious and low-key thing for car companies to adjust the official price guide. Even if suppliers increase prices, there is room for negotiation. Especially in the era of fuel vehicles where the “complete vehicle is king”, OEMs mostly dominate and even transfer the risk of price fluctuations to suppliers.

Taking a step back, even if the price is to be increased, car companies will use the method of increasing or decreasing the configuration to euphemistically and slightly eliminate the cost pressure. It is not common in the auto industry for car companies to group together to increase prices due to “upstream price hikes” like March.

The right to speak on pricing is shifting, which is the root cause of passive price increases by car companies. As the role of batteries and chips in automobiles becomes more and more important, car companies are not the only strong parties that dominate product prices, but also face upstream constraints such as battery factories and chip factories.

Taking power batteries as an example, in addition to BYD’s self-produced batteries, which can be self-supplied, CATL occupies more than 60% of the market. Although it is said that the CATL does not like the domineering title of “Ning Wang”, its strong position does bring more bargaining power. According to several media reports, the price of power batteries in CATL has increased several times. The price of power batteries has increased by more than 15% this year and will continue to increase in price negotiations in the next two quarters.

“Compared with increasing prices, everyone is more afraid that if there is no car to sell, the company will be finished. No matter how high the upstream price is, you have to buy it. We just hope that the supply can catch up sooner.” A staff responsible for purchasing a car company said that compared to the shortage of chips that has continued since last year, at least there is still “talk” about batteries.

“Now OEM (car companies) who want to open a second supply, who want to do (battery) by themselves, will not have a battery to get it. Whoever follows the head battery factory wholeheartedly and signs an exclusive supplier can get battery resources as soon as possible, even if the price rises outrageously.” An expert in the industry said, “Battery companies are forcing the overall price increase downstream.”

However, while battery companies are tough on downstream car companies, they are also under pressure from their upstream raw material suppliers to increase prices.

Lithium carbonate and nickel’s multiple folds of price increases are too outrageous for battery manufacturers. According to market rumors, CATL and BYD plan to “group together” to boycott upstream raw material suppliers, and collectively do not purchase lithium carbonate with an offer price of more than 500,000 yuan/ton. However, neither CATL nor BYD responded to this.

We believe that whether the high price of lithium carbonate will continue depends on the changes in the supply side. In the next few decades, the strong demand for resources such as lithium and nickel means that it is impossible for them to fall back to the cost level, and the regularity of cyclical fluctuations will fail. In a market that is in short supply, even if the downstream group boycotts, it is impossible for the price to fall to the previous level.

Guotai Junan’s research report said that the rapid rise in lithium carbonate prices was mainly due to the urgent demand for lithium carbonate due to the development of the new energy market, especially overseas energy storage batteries, which further increased lithium prices. Research institutions such as China Merchants Bank Research Institute, Deloitte, and some mining companies have predicted that the structural shortage of upstream minerals will be difficult to alleviate in the short and medium-term.

At the China Electric Vehicle 100 Forum last weekend, the price increase of new energy vehicles was hotly debated. Ouyang Minggao, vice chairman of the China Electric Vehicle 100 Association and academician of the Chinese Academy of Sciences, believes that the current round of power battery material price increases is basically the same as the lithium resource price increase in 2016-2018, but due to stronger demand and expected growth, coupled with the impact of the epidemic, the price volatility is greater. He expects that the balance of supply and demand of lithium resources may return to normal in 2-3 years.

Xin Guobin, Vice Minister of the Ministry of Industry and Information Technology, said that it is necessary to moderately speed up the development of domestic resources, resolutely crackdown on unfair competition such as hoarding, speculation, and speculation, and promote the return of key raw material prices to rationality.

In order to have more pricing power, car companies are also “upstreaming”. OEMs such as Wei Xiaoli, BYD, Volkswagen, and GAC New Energy are all deploying upstream raw material resources such as nickel and lithium to cultivate their own battery systems. Gu Huinan, general manager of GAC Aian New Energy Automobile Co., Ltd., said that car companies need to master battery technology and be able to achieve self-sufficiency in small batches.

Even so, for new energy car companies, the good days of enjoying subsidy dividends while leading the pricing strategy are over.